Whether you’re eyeing an exit or you’re curious what you’ve built, valuing a small business comes down to two numbers: what it earns for its owner and the multiple a buyer will pay for that. Get both right and you can put a realistic range on the business.

This guide walks the method step by step, with a worked example you can follow using your own figures.

The earnings number that matters for a small, owner-run business is SDE, and most of the work is calculating it honestly. From there you pick a multiple, then adjust for inventory, debt, and cash to reach what you’d walk away with.

An online business valuation follows the same path, and we’ll flag where ecommerce specifics move the multiple.

What is a small business worth?

A small business is generally worth its SDE, the total yearly financial benefit it gives its owner, multiplied by a figure that reflects its size, growth, and risk. Most small businesses sell for somewhere around 2 to 4 times SDE, and the price is then adjusted for inventory, debt, and cash to reach what the seller actually receives.

This earnings-multiple approach is how most Main Street businesses change hands. Asset-based and discounted-cash-flow methods exist, and they suit asset-heavy or high-growth companies, but for a profitable, owner-run business a multiple of SDE is what buyers and brokers reach for first.

Two things follow from that formula. Value is a range, not a single number: the same business can be worth more to a strategic buyer than to a first-timer, and the multiple flexes with how clean and transferable the business is.

And buyers pay for earnings they can verify, so the quality of your books does real work on the price you can defend.

What is SDE (seller’s discretionary earnings)?

SDE stands for seller’s discretionary earnings, the total financial benefit a single owner-operator takes out of a business in a year. It starts with profit and adds back the things that are really owner benefits or won’t carry over to a new owner: your salary, personal expenses run through the business, and one-time costs.

Small, owner-run businesses are valued on SDE rather than net profit because the owner’s pay and perks are a choice, not a fixed cost of running the business.

A buyer wants to see the whole pool of cash the business throws off before those owner decisions, so they can judge what it would earn under their own setup.

That’s why SDE, not the profit line on your tax return, is the number a small-business buyer works from.

Adding owner pay back also makes businesses comparable. Two stores with identical operations can report very different profits simply because one owner pays themselves twice as much. SDE strips that choice out, so a buyer can line up your business against others and judge it on the cash it generates, not on how you happened to draw a salary.

How to calculate SDE

Calculating SDE is a series of add-backs on top of your net profit. Work down your profit and loss statement and add back each owner benefit and one-off, and the total is the earnings a buyer will value.

The standard add-backs are owner compensation, discretionary and personal expenses, one-time costs, and interest, taxes, depreciation, and amortization.

Building SDE from net profit, one add-back at a time (illustrative figures).

| Line | Amount |

| Net profit (from your P&L) | $120,000 |

| + Owner’s salary and compensation | $70,000 |

| + Owner perks and personal expenses | $12,000 |

| + One-time, non-recurring costs | $8,000 |

| + Interest, taxes, depreciation and amortization | $15,000 |

| = SDE | $225,000 |

Not everything qualifies. A cost the business genuinely needs to keep running stays in, so the salary of an employee a new owner would have to keep, or ordinary rent and software, aren’t add-backs. The test is whether the expense would disappear or change hands with the sale.

One caution: buyers and their advisers scrutinize add-backs. Anything you add back has to be documented and genuinely discretionary or non-recurring. An aggressive add-back you can’t support gets stripped out at diligence, and it makes a buyer question the rest of your numbers, which costs you more than the add-back was worth.

SDE vs EBITDA: which one, and when

SDE and EBITDA both measure earnings, and they differ in one place: the owner’s salary. SDE adds a single owner-operator’s pay back in. EBITDA leaves in a market-rate salary for whoever runs the business.

That makes SDE the right lens for a small business the owner runs day to day, and EBITDA the right one for a larger business a buyer will run with a hired team.

The rough dividing line is size, and underneath it, owner dependence. Businesses with earnings up to around $1 million usually trade on an SDE multiple, those above roughly $2 million shift to EBITDA, and the band between is where buyers pick whichever metric fits.

If a buyer would have to replace you with a paid manager, subtract that manager’s market salary and you’re valuing on EBITDA. EBITDA multiples also tend to run higher than SDE multiples, which is part of why crossing that threshold matters.

Picking a valuation multiple

The multiple is where judgment comes in. Two businesses with the same SDE can carry very different multiples depending on how risky and transferable a buyer judges them to be. An online business valuation runs on the same method, with ecommerce-specific ranges we cover in the guide to valuing an ecommerce business. The factors that move the multiple apply either way.

Start from a base multiple in the low single digits and adjust from there. A steady, well-documented business earns its way up the range, while one that leans heavily on the owner or a single sales channel gets marked down. The table below sketches where different profiles tend to land.

Directional SDE multiples for small businesses, as of early 2026. Ranges vary widely by quality.

| Business profile | Typical SDE multiple |

| Very small, owner-dependent | ~1.5–2.5× |

| Established, stable earnings | ~2.5–3.5× |

| Larger, growing, low concentration | ~3.5–4× and up |

Within those ranges, these factors push a multiple up or down:

- Size: Bigger earnings command higher multiples, since larger businesses read as more stable.

- Growth: A business growing steadily is worth more than a flat or declining one.

- Profit stability: Consistent, predictable earnings earn a premium over lumpy ones.

- Concentration: Heavy reliance on one channel, supplier, or customer pulls the multiple down.

- Owner dependence: The more the business runs without you, the more a buyer will pay.

- Clean books: Verifiable financials raise both the multiple and the odds the deal closes.

From value to net-to-seller

The headline value isn’t what lands in your bank account. A sale price gets adjusted for what the business owns and owes at closing, and for how the deal is structured.

Add inventory at cost on top of the business value, since a buyer pays separately for the stock they’re taking on. Subtract any debt the business carries, and settle cash and a working-capital peg, the minimum working capital a buyer expects to find in the business on day one.

Deal structure matters too: part of the price may come as an earnout, paid over time if the business hits agreed targets.

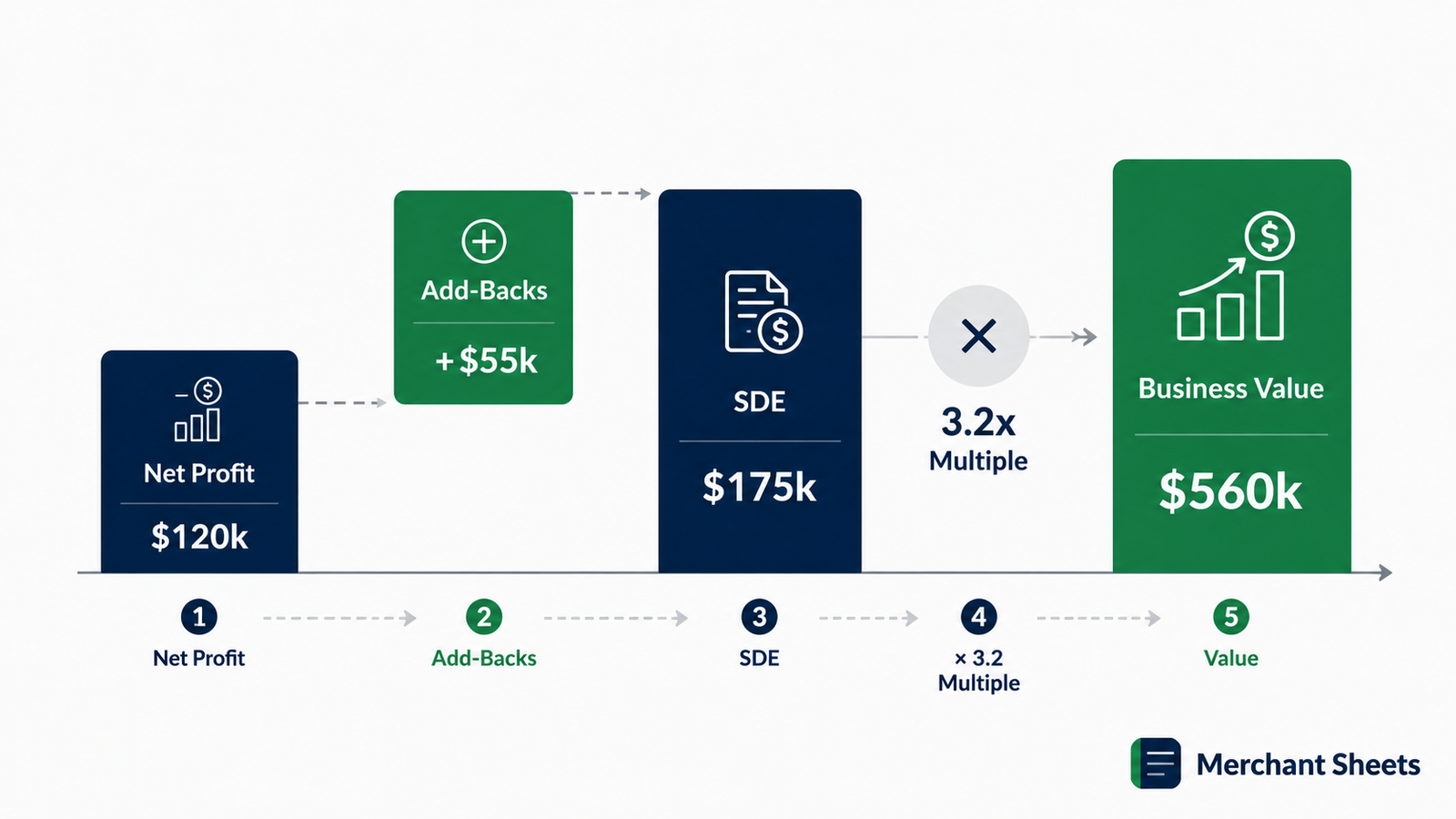

A worked example

Here’s the whole method on one business. Say a store nets $120,000 in profit, pays its owner a $70,000 salary, runs $12,000 of personal expenses through the books, had $8,000 of one-time legal costs, and shows $15,000 in interest, taxes, and depreciation. Work it through in four steps.

- Add up SDE: Net profit plus the add-backs comes to $225,000 in seller’s discretionary earnings.

- Pick a multiple: Stable earnings, low concentration, and clean books support a 3× multiple.

- Find the headline value: $225,000 × 3 = $675,000.

- Adjust to net-to-seller: Add $40,000 of inventory at cost, subtract a $30,000 loan, settle cash and the working-capital peg, and you land near $685,000 before deal structure.

Frequently asked questions

What multiple does a small business sell for?

Most small businesses sell for roughly 2 to 4 times SDE, though the range is wide and depends on size, growth, and risk. Smaller, owner-dependent businesses sit at the low end, while larger, stable, growing ones with clean books reach the top and beyond. Treat any rule-of-thumb multiple as a starting point, then adjust for the specifics of the business and its market.

Is SDE the same as profit?

No. SDE starts with profit and adds back the owner’s salary, personal expenses run through the business, one-time costs, and interest, taxes, and depreciation. The result is the full financial benefit the business gives its owner, which usually lands well above reported net profit. That larger number is what small-business buyers actually value.

Should I use SDE or EBITDA for my business?

Use SDE if you’re a hands-on owner running a smaller business, since it counts your salary as part of the return. Use EBITDA once the business is large enough that a buyer would run it with a hired manager, usually somewhere above $1 million to $2 million in earnings. When you’re in between, calculate both and see which a likely buyer would lean on.

Do I need a professional valuation?

For a rough sense of value, the method here gets you a defensible range. For a real sale, financing, or a dispute, get a professional valuation or work with a business broker who knows your market. A formal valuation carries weight with buyers and lenders that a spreadsheet estimate doesn’t, and it’s worth the cost when real money is on the line.

What your business is worth, on your numbers

The method here gets you a defensible range, and the work is in getting SDE right and picking a multiple you can stand behind. Both reward clean books and a clear head about what’s genuinely discretionary.

The Ecom Business Valuation Tool runs the whole process on your figures: it captures your add-backs, builds a multiple from a size-based starting point with factor adjustments, and reconciles to a net-to-seller range after inventory, debt, and cash.

See a defensible value for your business, and know the number before you ever take a call.