You can turn a profit on every order and still watch your bank balance slide. The reason is net working capital — the cash your business locks up in inventory and unpaid invoices before it comes back to you. Reading it well is the difference between growth that funds itself and growth that quietly drains your account.

This guide covers what net working capital is, the formula in both its textbook and operator forms, why it tightens exactly when you’re growing, and the levers that free the cash back up.

It sits at the heart of your cash flow forecast, and it’s one of the most misread numbers in ecommerce.

What is net working capital?

Net working capital is what a business has left after subtracting what it owes in the short term from what it owns in the short term. The formula is current assets minus current liabilities. It measures the short-term liquidity you can put to work, and for most stores, most of it is cash sitting in inventory and unpaid invoices.

Current assets are the things you’ll convert to cash within a year: your cash on hand, inventory, and accounts receivable (AR), the money customers or channels still owe you.

Current liabilities are what’s due within a year, chiefly accounts payable (AP), the money you owe suppliers, plus any short-term debt. Subtract the second from the first and you have your net working capital.

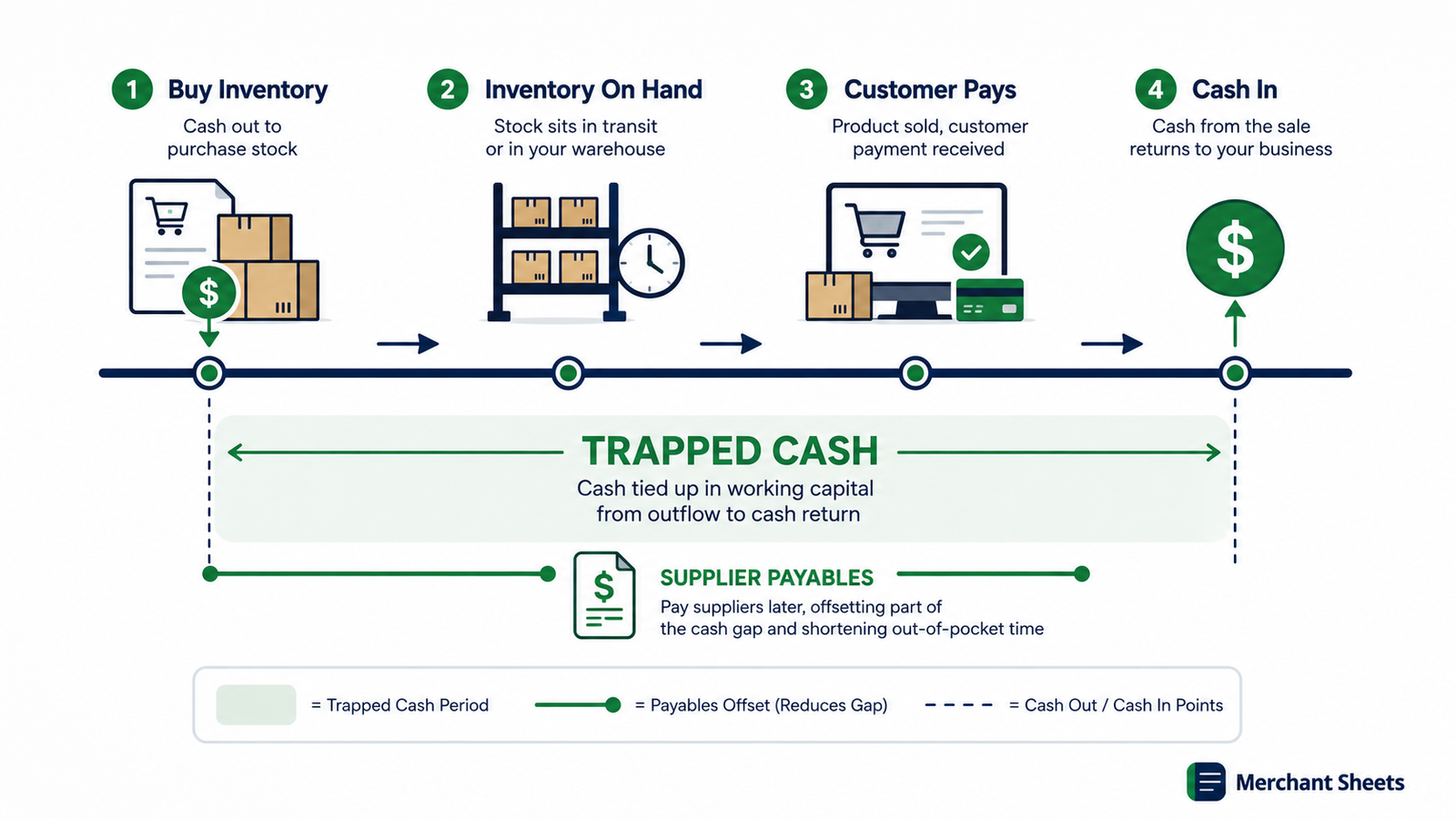

A positive number means your short-term assets cover your short-term obligations with room to spare. That room is also the catch, because much of it isn’t spendable cash. It’s stock on shelves and invoices you’re waiting to collect, which is how a healthy-looking working capital figure can sit right next to an empty checking account.

It helps to hold two lenses at once. The balance-sheet view — every current asset minus every current liability — tells you whether you could cover near-term obligations if you had to.

The operating view zooms in on the working capital your day-to-day trading creates: stock, what customers owe you, and what you owe suppliers. The first is a solvency check; the second is where an ecommerce store’s cash gets trapped and freed.

The net working capital formula

Two versions of the net working capital formula are worth knowing. The textbook one works off your balance sheet; the operating one strips it down to what ties up an ecommerce store’s cash.

Net working capital = current assets − current liabilities

Operating net working capital = inventory + accounts receivable − accounts payable

The first is the full accounting view. If your balance sheet shows $180,000 in current assets and $120,000 in current liabilities, your net working capital is $60,000.

The operating version drops cash and short-term debt to isolate what your operations tie up. Say you hold $80,000 in inventory, $20,000 in receivables, and owe suppliers $40,000.

Your operating net working capital is $80,000 + $20,000 − $40,000 = $60,000 locked in the cycle of buying stock and collecting on sales.

For a cash-up-front DTC store, receivables are small because customers pay at checkout, so inventory and your supplier terms drive the number. For a brand selling wholesale on net-30 or net-60, receivables swell and become the bigger lever.

Same product, different cash tied up: operating net working capital by store type

| Store type | Inventory | Receivables | Payables | Operating NWC |

| DTC (cash at checkout) | $80,000 | $2,000 | $40,000 | $42,000 |

| Wholesale (net-60 terms) | $80,000 | $70,000 | $40,000 | $110,000 |

Same inventory and the same supplier terms, and very different cash tied up. The wholesale brand’s net-60 receivables lock up an extra $68,000 against the DTC store that collects at checkout. Identical product, identical margins — the terms you sell on decide how much cash the model strands.

Where net working capital sits on your balance sheet

Both formulas read off the same place: the top of your balance sheet, where current assets and current liabilities live. Here’s the $180,000-and-$120,000 example broken out.

The current assets and liabilities behind a $60,000 net working capital

| Current assets | Amount | Current liabilities | Amount |

| Cash | $80,000 | Accounts payable | $40,000 |

| Inventory | $80,000 | Short-term debt | $80,000 |

| Accounts receivable | $20,000 | — | — |

| Total current assets | $180,000 | Total current liabilities | $120,000 |

The accounting formula nets those totals to $60,000. The operating version strips out the $80,000 of cash and $80,000 of short-term debt, leaving $80,000 in inventory plus $20,000 in receivables minus $40,000 in payables — the same $60,000, now framed as the cash your trading cycle ties up.

When cash and short-term debt are close in size, the two figures land together; when they diverge, the operating number is the one that tracks your cash.

Why does net working capital make or break cash?

Net working capital makes or breaks cash because of how it changes, not what it is at any one moment. When your net working capital rises, cash leaves the business to fund it; when it falls, cash comes back.

Growth is what pushes it up — more sales pull more cash into inventory and receivables before that cash returns.

Picture a quarter where sales climb. To meet demand you buy more inventory, so your stock balance grows. Customers and channels owe you more, so receivables grow.

Your suppliers extend some credit, so payables grow and offset part of it. The gap is cash that has left the building.

How a profitable quarter can still drain cash

| Working capital account | Change over the quarter | Cash effect |

| Inventory | +$50,000 | −$50,000 |

| Accounts receivable | +$30,000 | −$30,000 |

| Accounts payable | +$20,000 | +$20,000 |

| Change in net working capital | +$60,000 | −$60,000 |

That $60,000 rise in net working capital is $60,000 of cash absorbed over the quarter, even if the P&L shows a healthy profit. The profit is real; it’s sitting in boxes and invoices instead of your account.

This is how growing, profitable stores run short of cash, and why a big inventory buy right before a slow wholesale season can leave you scrambling.

Ecommerce makes the trap sharper than the textbook version. Overseas suppliers often want a deposit when you place the order and the balance before it ships, so cash goes out weeks or months before a single unit sells.

Stack a peak-season inventory build on top of marketplace payout lags, and net working capital can swing hard in one quarter — the exact quarter your sales chart looks its best, which is why fast-scaling brands so often reach for financing right when the business looks healthiest.

Scale those swings up and the stakes get real. A brand adding $260,000 to net working capital in a quarter to fund a growth spurt has spent a quarter of cash it won’t see back until the inventory sells and the invoices clear — profitable P&L and all.

That’s the moment many operators find their reported profit and their bank balance have almost nothing to say to each other, and it’s why cash, not profit, is what runs a store aground.

Two other numbers describe the same squeeze from different angles. The cash conversion cycle measures it in days — how long your cash is tied up between paying for stock and collecting on the sale.

And the change in net working capital feeds straight into free cash flow: a rising balance is a direct drag on the cash your business generates.

Seeing a $60,000 swing before it lands is the whole point of a rolling forecast. A big inventory order or a slow-paying channel shows up as a tight week in the 13-Week Cash Flow Forecast, so a working-capital squeeze becomes a date on the calendar instead of a surprise.

How much cash will your growth tie up?

You can estimate the cash a growth push will consume before you commit to it. Net working capital tends to scale with sales, so measuring it as a share of revenue — a working-capital-to-sales ratio — gives you a planning multiplier: each extra dollar of sales ties up roughly that share in inventory and receivables, net of supplier credit.

Say your net working capital runs near 20% of sales. Plan to grow revenue by $500,000 over the next year and you’re signing up to fund about $100,000 of additional working capital along the way, cash that goes out before the new sales pay it back.

Knowing that figure ahead of time turns a growth plan into a financing plan: you decide up front whether the cash comes from profit, better supplier terms, or a credit facility, rather than hitting the gap mid-scale.

The ratio also points at the fix. A high number driven by inventory sends you to your reorder discipline; one driven by receivables sends you to your terms. Track it each quarter and it tells you whether growth is getting more cash-efficient or less.

Positive vs negative working capital

Most stores run positive net working capital: more is tied up in inventory and receivables than they owe suppliers, so cash sits in the operating cycle.

Negative working capital flips that — you collect from customers before you have to pay suppliers, so the business runs partly on other people’s money and funds its own growth.

For a typical inventory-led store, some positive net working capital is normal and even necessary — you need stock on hand to sell and a buffer to pay suppliers on time. The goal isn’t zero; it’s keeping the number from creeping up faster than sales as you grow.

A few ecommerce models reach the efficient extreme structurally: a marketplace seller paid out quickly while riding supplier terms, or a subscription brand that charges upfront for products it fulfills later.

Negative working capital isn’t automatically good or bad. It depends on where it comes from:

- Healthy negative working capital: It comes from fast inventory turns and cash-up-front sales, like a marketplace or subscription that collects at checkout while paying suppliers on net-30. The float funds growth.

- Warning-sign negative working capital: It comes from stretched or unpaid suppliers and falling sales, where payables balloon because you can’t pay on time. It looks the same on paper and means the opposite.

How do you free up cash tied in working capital?

You free up cash by shrinking the gap between paying for inventory and collecting on sales. The money is already yours; it’s stuck in the cycle. Which lever matters most depends on your model — inventory for a DTC brand, receivables for a wholesaler — and freeing this cash is one of the cheapest ways to extend your runway, since it’s cash you earned rather than cash you borrow.

Three levers do the work:

- Turn inventory faster: Inventory holds the most working capital in an ecommerce store, so every extra week of stock on the shelf is cash you can’t use. Tighter reorder discipline and clearing dead stock let you turn inventory faster and carry less of it.

- Stretch supplier terms: Every day you delay paying a supplier is a day that cash stays in your account. Moving from net-15 to net-30, or negotiating deposits down, widens payables and shrinks the cash gap.

- Speed up what you’re owed: Faster marketplace payouts, shorter wholesale terms, and prompt-payment incentives pull cash in sooner. For a DTC store this lever is small; for a wholesale brand it’s often the biggest one of all.

See the squeeze before it lands

Net working capital only becomes a crisis when it catches you off guard. A profitable quarter that quietly eats $60,000 of cash is manageable if you see it coming and a scramble if you don’t.

The 13-Week Cash Flow Forecast maps your weekly cash in and out and carries each week’s balance into the next, so a big inventory buy or a slow-paying channel shows up as a tight week before it lands.

Frequently asked questions

What’s the difference between working capital and net working capital?

They mean the same thing in practice — both are current assets minus current liabilities. Some people say “working capital” loosely for the general idea of short-term liquidity and “net working capital” for the precise figure, but the calculation is identical, so a working capital number almost always refers to the net amount.

What’s a good net working capital ratio?

A current ratio — current assets divided by current liabilities — of roughly 1.5 to 2.0 is the common rule of thumb, meaning you hold $1.50 to $2.00 in short-term assets for every $1.00 you owe. For an inventory-heavy ecommerce store, a high ratio can mean cash is trapped in stock, so weigh the quality of the assets, not the level alone.

Does net working capital include cash?

The accounting figure includes cash, since cash is a current asset. The operating version used to gauge how much cash your business ties up leaves out cash and short-term debt, isolating the inventory, receivables, and payables that move with operations. Which one to use depends on the question: total liquidity, or cash trapped in the cycle.

What is change in net working capital?

Change in net working capital is the difference in your net working capital from one period to the next, and it’s the part that moves cash. It’s recorded on the cash flow statement as a use of cash when it rises and a source of cash when it falls. The level tells you how much is tied up; the change tells you which way cash is flowing.

Is negative working capital bad for an ecommerce business?

Not necessarily — negative working capital can signal an efficient model when it comes from collecting cash before you pay suppliers, which is common for marketplace sellers and subscription brands with fast inventory turns. It’s a problem when it comes from the other direction: falling sales or an inability to pay suppliers on time. The cause matters more than the sign.